-

I Just Bought a Utility Stock… Should You?

October 2023 Newsletter

Did I really buy a Utility stock? Yes, I did! Good investors must be able to adjust their approaches as the market evolves. For the last decade, I avoided utilities because I figured that they were at risk due to historically low interest rates. Interest rates were bound to reverse any time… said me ten years ago. I was recently proven right, but was it a good strategy to avoid an entire sector for a decade? Maybe not.

Are Utilities Bad Stocks?

There are stocks I typically do not invest in. A good example is Gold stocks; they are bad investments with low average returns, long wait times, etc. Then there are forestry stocks, which I refuse to buy because I like trees and do not like how these companies manage forests. You might think that the utility sector would be in the same permanent penalty box. Unlike my other 2 examples, there is nothing inherently wrong with utilities other than their sensitivity to interest rates. Every sector has their own characteristics, some good, some bad. There is no reason to exclude these for such long periods of time from a portfolio.

Utilities 101

Let’s start at the beginning for those of you who may not know what a Utility stock is. For the most part, utilities are exactly what they sound like when you think of paying your bills: electricity, natural gas, water, sometimes sewage, garbage disposal, and recycling to some extent. The big players however tend to be energy related.

Utility companies generally do not have a lot of growth. They simply sell you electricity (as an example), make a profit doing so, and then share most of it with their shareholders, reliably, year after year. The model is simple, yet kind of old world restrictive. Unlike Google, which simply rents office space for its employees, utility companies must build and maintain very expensive and complicated infrastructure to operate their business. Business expansion occurs slowly as the companies generally have to borrow to raise capital; its not an easy business and is often government regulated, which caps profits.

You do not hear much about them in the news because they represent less than 3% of the SP500 index. They are a small boring player in the economy so it’ easy to forget them. You can see why I avoided these for so long.

Why Are They Like Bonds?

Since Utility stocks pay reliable dividends and don’t grow very much, their stock prices act much like bonds. They are not all that different, especially if there is little business growth. As I have said in the past, stock prices are a function of supply and demand, always. If interest rates go up to today’s 5% level for example, then your reliable utility dividend rate of 3% is no longer competitive against a risk free bond. Why would anyone take a risk on a company with no growth offering 3% when you can get 5% risk free? Their stock price must fall drastically so that the dividend yield becomes competitive again. Simple economics.

Performance

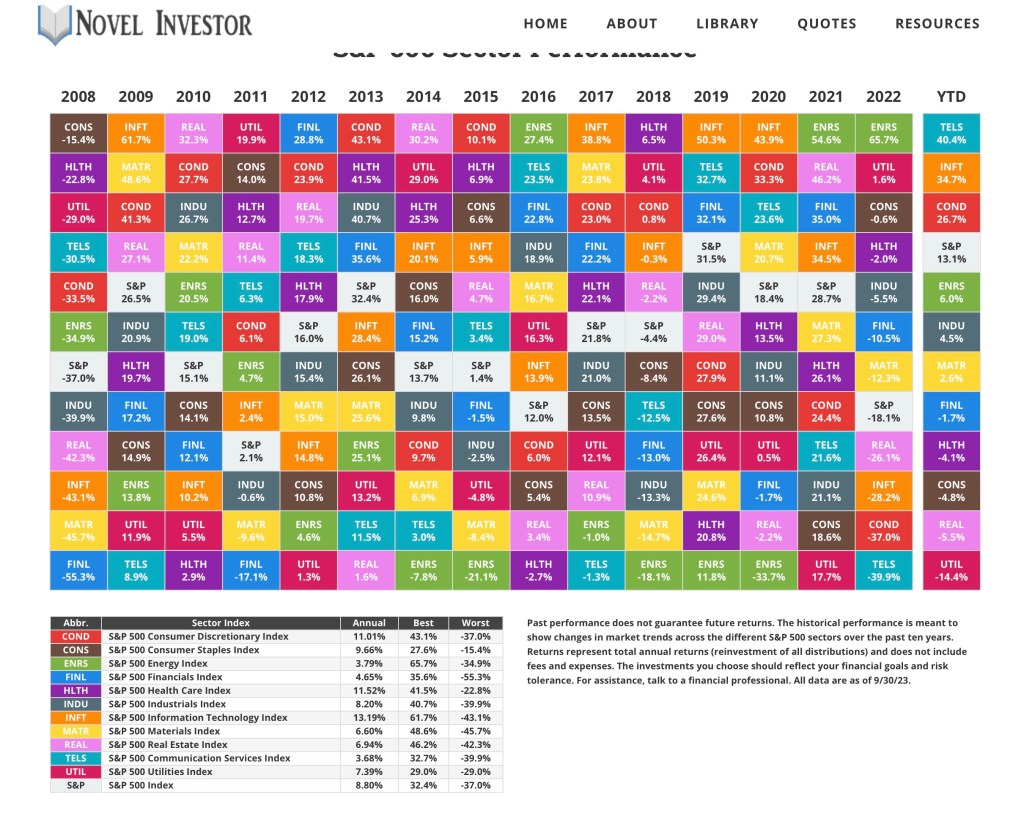

As it happens, Utilities are the worse performing sector in the SP500 index this year (-14%), they were also the worst (-17.7%) in 2021. It’s mostly because of rising rates. See Novel Investor image below for the latest sector performance for the last 15 years. Be aware that it’s not all bad news, they have had some very good years.

Relative to other sectors, Utilities rank around the middle. While the SP500 returned 8.8% over 15 years, utilities returned 7.4%. If you take into account risk and some pretty bad recent Utility Sector returns, overall that’s pretty good. Information Tech on the other hand returned 13%, which is amazing, but it has become a very expensive (read risky) sector. Its’ oversized effect on the average SP500 return is also worrisome. If you took the information Tech sector out of the index, Utilities would likely be neck and neck with the average.

Was Shunning Utilities the Right Strategy?

If rates started rising years ago, then certainly the “shun utilities” strategy would have been dead on. Investing is all about probabilities and not certainties, there is always a great deal of randomness involved. Even if something is likely to happen (rates go up soon), they simply may not. Nothing is certain, just different levels of probability. You’re best to play the odds, knowing that you can be wrong sometimes. This is what makes investing interesting. How often does one of your good for nothing stock picks double or triple, while your highest conviction “sure thing” pick drops in half? Happens all the time.

Time to Buy?

So is it time to buy Utilities? Honestly, I do not know. Simply speaking, you would need to know where interest rates are headed. If you knew that, you could bet everything you owned and become super wealthy. No one really does this because no one really knows, and neither do I. What I do know is that rates have climbed from basically zero to about 5% – the highest levels in 16 years. That is huge and the utility sector has been devastated. But just because rates have gone up a lot, it does not mean that they can’t continue going up. Rates were increased to about 20% in the early 80s to combat inflation, a similar situation is happening now.

The New Strategy

So my reasoning for buying, rightly or wrongly, is that lots of risk has been removed from utilities. Could rates go up and continue pounding utilities? Yes. So I have taken a half position with the idea that if rates keep going up and utility stocks keep falling, I will simply buy more until I achieve a 3% portfolio weighting. There are other less obvious but more important benefits for making the purchase. In my case, I have to consider portfolio management where diversification plays a key role in returns. The purchase increases diversification with the side benefit of lowering overall volatility. In addition, Utilities in the right context make a great defensive position should a recession come along.

Ok, So Which One?

After looking at hundreds of utilities stocks, I have to say that generally these are not the kind of companies that I would historically invest in. There are high yield 6-10% companies that are in my opinion “attractive but dangerous” because they have too much debt and are suffering from high borrowing rates. Most of the companies have very little opportunity for growth and those who have growth, are more expensive. You kind of get what you pay for in Utilities. My advice is that in the long run, you’re better with a lower yield (under 6%), a bigger company, some growth, increasing dividends annually, long history of dividend payments. These companies fared much better than other lower quality companies with bigger initial yields and as such, prices reflect that.

I eventually bought Fortis (FTS), a Canadian company that provides electricity and gas to customers in Canada, USA and the Caribbean. It’s a big player with a 26 billion market cap, and is considered the gold standard in Canada. It’s not particularly cheap, but it has growth opportunities which makes up for this. Its dividend yield is 4.4 % and has been increasing these annually for the last 50 consecutive years. In the short term, dividends are expected to grow at a rate of 6% per year. If you’re into Beta (a volatility measure), it scores a super low 0.23.

Something Has to Go

With a new sector being added to the portfolio, something had to be paired down. My energy sector positions have done so well that they became overweight. It makes it easy to move around money when this situation exists. While I was at it, I sold off MSOS a speculative Marijuana stock (small position) which did not work out, as well as a small cap ETF (VSS) which is too small to be relevant.

Marc’s Monthly Moves

- Sell half of Shell (SHEL) (+103% return)

- Sell MSOS (-73% loss)

- Sell VSS (+7% return)

- Buy Fortis (FTS)

Marc’s Portfolio YTD Performance

- Portfolio return: 9% (including currency gains)

- Portfolio return: 7.8% (without currency gains)

- S&P 500 return: 10%

- RSP ETF S&P equal weight -3%

- TSX: -1.4%

When Will this Under Performance End?

The portfolio has under performed the S&P 500 by 2.2% percentage points. I always get concerned about any deviation over 2%. Since I have moved further away from a USA heavy weighting, I believe that I am at a disadvantage to keeping up with the index. As long as a few very expensive market leaders continue to lead, I will likely not be able to keep up. The consolation prize is that the portfolio is less risky. It will likely over perform when the market finally realizes its wicked ways.

-

Is Frugality a Super Power?

I did not retire in my late 40s simply by making loads of money or by being a whizz at investing, contrary to what most people think. In the beginning like most, I kind of sucked at investing and my returns were all over the place. Also like most, I didn’t make a lot of money at the beginning of my career; it took years to build up my salary and eventually became above average as I entered management level. Even so, were talking a public service government job, decent pay, but no jets or Ferraris… a normal income.

The biggest contributor to my early retirement was frugality – always being careful with money. Don’t get me wrong, maximizing your salary and investment income is necessary, as you need something to work with after all. But managing money ties it all together. It’s actually very basic, yet so difficult to achieve for most. You simply need to spend less than you make, invest the difference wisely, get the snowball rolling and let time take care of the rest. That is the secret sauce and its available to most everyone.

So why is it so difficult to implement a basic money management plan? There are so many reasons the odds are stacked against you. Let’s just touch on a few obvious ones: Money management is not taught in school, which is kind of odd right? You get out of school being able to solve a 3 sided triangle but know nothing about investing. The next problem is that you are bombarded with hundreds of ads a day trying to make you buy something you do not need. Add to this, most everyone around you drank the Kool Aid and now have shiny new things. The pressure is everywhere and its super difficult to resist all temptations. I bought a 20-year old corvette in my 20s, which was really fun, but financially stupid. No one is immune to consumerism, its always around us, but it needs to be managed. Let’s face it, without consumerism, life would be boring, we would live in hovels wearing old potato bags and shoes made of old tires. Not quite a life for most, even me. There has to be some acceptable balance where you can still buy fun things, do fun things, but yet still retire early enough to enjoy other fun things.

So is frugality a super power? Not really. The super power is more in the attitude necessary to truly make frugality effective. The “I do not care what others think” is really what can liberate you from society’s grip. The kind of car you drive, the clothes you wear, the house you live in, etc. I am pretty sure people thought I was weird as most everything I did was different than everyone else. For every purchase, I had an automatic check of: do I really need it?; can I buy it used; can I make it? To this day, even though I am retired, I still follow these rules. A simple example that demonstrates this attitude recently came up while I was traveling through Mexico. It was the use of helmets while rock climbing. My girlfriend just laughs as everyone else has these fancy specific rock climbing helmets while I wear my cycling helmet. It’s a helmet, right? So I do not need another. I apparently look kind of funny… but I do not care. Super Power? Maybe…

The Small, the Big and the Stupid

There are a lot of resources about how to be frugal and this article is not really about that. What I am trying to focus on here is the concept and the power of harnessing frugality and the attitude that you need to make it work. To do it in a big way, you need to be good with people thinking you are a weirdo. Winning this game is about staying on top of small potentially reoccurring expenses like lattes or cable tv and big items like cars, boats, and homes. Many of these purchases are unnecessary, but masked as life necessities (do your really need a 3000 sqft home… some actually do… most don’t). Avoiding stupid mistakes on these big financial decisions have big benefits to your future because of the time value of money. Every dollar saved early in life can compound and snow ball into huge sums.

Let’s start with the small things… Eating out! For the most part, I was very good at bringing my lunch to work and mostly avoided buying junk food at the cafeteria. I remember several occasions over the years where coworkers would question why I did not buy a coffee or snack. I would normally start talking about compound interest etc… and there you go, I am the weirdo. There was a year where things got really busy at work and I actually started grabbing a meal every day at the cafeteria. I thought it was great and now could see how cool this eat at work culture was. I was making more money and my new work lifestyle reflected it. At the end of the year I tallied up what eating a quick lunch cost…WTF, 4000$. OMG I could not believe how this could be so much, and to make matters worse, that did not include eating out on weekends. I also gained over 25 lbs. I put a stop to all that, and became a weirdo again.

The next example is about the big things like cars. I really like cars, especially sports cars, but I know that cars are an expensive depreciating asset. Even though I like cars, I have never bought a new car, ever, and likely never will. Again, there are plenty of websites on frugality, the point here is being able to do your own thing regardless of what everyone else does. Because I refuse to buy new cars, you will often see me driving cars anywhere from 10 to 20 years old. I have had many towed to the scrap heap over the years. One day, at work, there was a need to transport some of my employees to an afterwork social event. Oddly only a few people had their vehicles with them that day so we were a little short for carpools. So I said no problem and walked 15 minutes to my cheap monthly parking spot and retrieved my 15 year old Toyota Tercel. One of my up and coming employees mentioned that this is not the car that he envisioned someone at my level driving. He paused, then said, and I quote “you do things differently don’t you…you know that is really smart”. Then he went on to defend why he just bought a new car. A decision which mostly revolved around the safety requirements necessary for having a child.

I guess I need an example of the fun/stupid. Well let’s go back to that corvette I bought in my early 20s. It was an emotional purchase, expensive and not in line with my frugality at all. Not only that, had I researched it more, I would have bought a better model that at least could have increased in value over time. Luckily, that purchase was short lived as I needed the money go back to university, so i did manage to resell it at a somewhat reasonable loss. But this could have been much worse. Everyone makes mistakes, and these need to be minimized as much as possible. Our emotions are always working against us when it comes to the forces of consumerism.

How happiness is the answer

The earlier one can break away from society’s expectations, the easier it is to build wealth. The three examples that I provided have made a big difference in my life with little if any loss to my happiness during that time. There are many more things I did that also contributed to this approach, and I may touch on these in another article, but these three are the biggest ones. People simply need to stop spending everything they make since it does not make them happier. For most people, getting away from work and spending time doing what they love is the answer.

There is a balancing act where you must be comfortable with living now and living later, and that is entirely a personal one. Some people are quite happy to work and spend everything they have knowing that they will need to work until they are in their mid 60s or later. I have no problem with this, if this is what they truly want. I could have easily retired in my early 40s had I not travelled to Europe so much, or built my first house or bought the stupid corvette. Again, life would be boring without spending money and experiencing it when you’re young. The right balance is tricky and personal. My message here is that it’s fine to spend money as long as you achieve your financial goals and do not end up old, poor, and alone. In the end, everyone has to figure out how to be happy in life and the sooner they realize that it has little to do with how much much money they spend per month, the better off they will be. Beware, however, that taking a step away from the consumerist system will make you a weirdo but at the same time it will free you from all of societies expectations.

-

What You Need to Know About Crypto Currency

As an investor with an economics background, I’m fascinated by cryptocurrency. It’s an innovative form of currency that differs from anything the world has seen since the development of modern money. Crypto isn’t tied to a specific country, it’s digital, it’s not easily manipulated, and is backed by complex technology. What’s even more interesting to me is its meteoric rise, and fall, and the willingness of people to invest huge sums of money in it without fully understanding the currency and its risks.

In this post, I’m sharing what you need to know about cryptocurrency (it’s not what you expect!) and guidance for investing in it going forward.

Crypto Currency Is Speculative

Crypto is speculative due to its high volatility. Any investment that can go up that fast can easily come down just as quickly. It’s also speculative due to the hype that surrounds it. Discussions around crypto are consistently filled with unjustified conviction that it’s the best thing since sliced bread. This opinion was reinforced as the price of crypto kept gaining month after month, year after year. It had all the features of a bubble. When crypto was at its peak I stopped preaching to people about the risks as it seemed that no one wanted to hear it. I was that guy at the party who was bumming people out. At that time, there were only a few big holdouts, including Warren Buffett and Charlie Munger of Berkshire Hathaway. Charlie went so far as to call crypto “rat poison”.

One of the reasons crypto became so popular, in my opinion (leaving rising values aside), was that it is an anti-FIAT currency, in other words, crypto is a currency that is not managed and backed by trust in the government. It does its own thing without interference. Today, almost all currencies are backed by nothing more than the trust in government. For those who believe that their national currency is manipulated by an evil government, with absolutely no discipline in spending money, crypto is very appealing. It’s touted as a currency for the people, with no government control or regulation; essentially like crowd-sourced money for the people. It has a cool algorithm that limits the number of coins mathematically and its technology is impressive making it very tamper-proof.

Crypto Currency Likely Can’t be the New US Dollar

Currencies need to be manipulated and regulated. This isn’t a popular opinion but in economics, it is true. The great depression of 1929 was a big turning point in how governments managed economic shock. For the most part, governments do not want to be heavy-handed, they want to keep things stable. During the Great Depression, the government’s laissez-faire approach to managing currencies prolonged a down cycle that lasted a decade, and people suffered. If that’s too ancient history, look to the recent COVID-19 pandemic. Manipulation and intervention was the key strategy to saving the world economies. The current view is that the government (central banks) needs to intervene in situations where the economy cycles down too fast or conversely cycles up too fast. There are a number of ways that the economy can be throttled up or down. Without getting into complex mechanisms, this is mostly accomplished by adjusting interest rates and the money supply. Although not perfect, the economy generally gets pushed or pulled in the right direction.

Why the distrust in governments? That is a complicated issue, but it’s also rooted in history. There are plenty of examples of currencies that died at the hands of greedy businessmen and politicians. The ability to print as much currency as desired, without a limit or tie to something real (like gold or silver) has sometimes resulted in serious abuse. If too much money is printed, it eventually becomes worthless. This happens frequently in other countries. Even in the USA and Canada, crypto fans anticipate the demise of the US dollar, which will usher in a new era for crypto. There is some intuitive validity to the expectation that major currencies will eventually come crashing down because governments have been overspending year after year. It’s an interesting theory and it grabs headlines, but is it true? Not necessarily.

Crypto Currency Vs. Other Currencies

Most people do not realize that money isn’t a physical thing, it’s more like a concept or idea. Prior to money, people raised rabbits, then went to the local market to barter for carrots or fish (for example). The barter system was simple but the world moved very slowly and was for the most part very poor. The move to money was like discovering fire, a huge leap in the history of mankind. Money is a human construct that required the participation of and acceptance by society that money was an acceptable exchange medium. Because it’s a construct and not a physical thing, money can take any form. Throughout history, people have used shells, beads, cigarettes, playing cards, pantyhose, gold, silver, gold certificates, coins, and later paper currencies backed by gold, and finally FIAT currency, which is what we have today and is backed by nothing. It can be backed by nothing because it is ultimately very a powerful concept or idea.

So what currency was ever real? Answer: none of them. They are all human constructs, including gold. They are all based on the idea that as a society, we have valued and accepted (insert money type here) as a store of value, a unit of exchange, a unit of account, with a certain amount of confidence that it will not disappear overnight. But how can gold not be real? It’s shiny and has been around for thousands of years? It’s valuable! Well, it’s only valuable if we all agree that it is. If you think about it, gold is only useful to society to meet a few manufacturing needs – the rest is for jewelry, which is cultural and subject to change. Aluminum is a much more useful product and at one time more valuable than gold because of how difficult it was to produce (scarcity).

What you should take away from this article is that no currency, whether it’s gold, your bank account, or crypto, is real. Even if your favorite currency is backed by something (gold), it does not mean it’s more real. The system works on confidence and nothing more. It’s truly amazing. The existing monetary system has evolved over the last few centuries to become very complex and few people truly understand how it all works. It does not however stop everyone from having all kinds of opinions about how it should be managed. Central banks can make some dumb decisions about the system, mostly because it’s so complex, even with all their experts at their disposal, but they for the most part generally try and keep things stable by doing very little.

How does crypto fit into the monetary system? People have given it value, but stability is something it has never had. So it competes against other unstable currencies of the world with one big difference, it is not associated with a country. From an economist’s perspective, it’s genuinely fascinating. Crypto is much more comparable to gold except it’s electronic, it does not need to be mined or physically stored. The environmental aspects of mining crypto aside (it uses a huge amount of electricity to mine), it’s a much better version of gold.

Guidance for Investing in Crypto Currency

Investing in crypto has always been a bet that the existing reserve currency (the US Dollar) would fail and be replaced by crypto. Or at the very least crypto’s adoption would continue to grow and become one of the few major accepted currencies. It’s possible, but is it probable? No one knows if the US dollar will fail, and even if it does, why would it be replaced by crypto? Why not a new US Dollar, the Euro, the Chinese Wan, a US government digital dollar, or a multi-country led cryptocurrency? How likely is it that the powers competing for the reserve currency of the world would back crypto? They would have to give up the ability to manipulate the currency for good reasons (or for those conspiracy theorists for bad reasons). Like many things, it is possible that crypto does succeed and just like winning a lottery, if you are right, you win big. But even if this scenario plays out, you still have to figure out which cryptocurrency will be the winner. There are the obvious big players, but there are thousands to choose from and the majority of these will fail and fall into obscurity.

As long as investors understand that crypto replacing major currencies is a low-probability scenario, with a potentially high payout, there’s no harm in speculating. I would love to have held some crypto early on as a 1-2% weighted speculative bet. However, I was likely betting on something just as speculative at the time, which did not fair as well. That’s the way the investment cookie crumbles sometimes and that is ok.

I don’t think crypto is going away anytime soon, but it sure has lost some confidence. Will it shine again? Maybe, but the probabilities are not good. In any case, there is much to learn by following the cryptocurrency story.